OPTION LAB • EXTRA RETURN

BEYOND THE

BANK LIMITS.

Why the 6% "Bank Cap" is killing your returns.

Most retail investors are stuck with ETF investments or bank-issued "Structured Notes". They accept the passive return of the market or a mathematical ceiling: on a broad index like the S&P 500, static products rarely exceed a 6% annual yield. We call this the "Retail Trap". Relying instead on pure market return may lead to huge drawdown.

The Objective: Capturing 5%-7% monthly yield through quantitative analysis and active risk management.

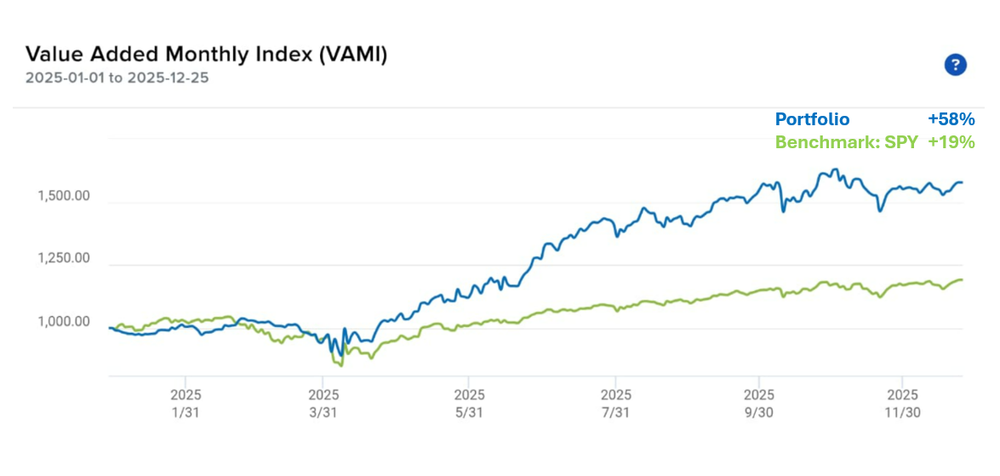

2025 Audited Performance

Real-money execution on SPY / US Blue Chips Portfolio

"Consistent returns are not about predicting the future, but about managing the Greeks. In 2025, our strategy generated a Sortino Ratio of 2.57, proving the superiority of risk-managed options over passive buy-and-hold."

"Wealth isn't found in a bank contract—it's built in the workshop."

Institutional Lab

STRATEGIC FRAMEWORK

Our approach reverses the standard banking paradigm. Instead of being passive market participants, we engineer outcomes. We replace the rigid barriers of retail structured products with **dynamic option architectures**, optimizing capital efficiency through **Asset Substitution** while eliminating institutional friction.

We exploit time decay (Theta) and volatility regimes (Vega) to extract consistent yield, regardless of broad market direction.

Unlike "all-or-nothing" barriers, we manage risk in real-time by adjusting Delta, ensuring a flexible defense even during high-stress volatility spikes.

The Result: A proprietary optimized structure that captures significant premiums in favorable markets while maintaining a defensive posture during crashes. True protection isn't a barrier—it's active control.

Strategic Design

The structure is built as an Optimized Diagonal Spread, engineered to reduce directional dependency and minimize active management overhead. High-yield positions often require adjustments; here, we target a statistical edge through Theta (time decay) differentials.

Selecting a 1-year LEAPS expiration stabilizes the position: acting as a proxy for the underlying stock with minimal capital outlay. Simultaneously, we sell 1-month Short expirations to capture accelerated time decay, generating a net credit and securing a Vega hedge during volatility spikes.

Desk Selection Parameters (SPY @ $694)

- → The Asset (Long): Dec 2026 Call | Strike $690 (0.60 Δ) | Cost: $5,960

- → The Yield (Short): Feb 2026 Call | Strike $705 (0.30 Δ) | Credit: $442

- → Capital Efficiency: 74% savings vs direct equity purchase

- → Target Monthly Yield: ~7.4% on invested capital

Dynamic Management: 3 Execution Scenarios

📈 Bullish Scenario (SPY > $705)

If the market accelerates, we monitor directional drag.

Desk Action: We execute a Roll Up and Out to restore positive Delta and harvest higher premiums.

⏳ Neutral Scenario (SPY $690 - $705)

The ideal scenario for cash flow. The Short Call expires worthless.

Desk Action: We harvest the $442 premium and systematically drive the cost basis toward zero.

📉 Bearish Scenario (SPY < $690)

The Short Call cushions the downside. We monitor the 0.40 Delta floor strictly.

Desk Action: If the threshold is breached, we close to preserve principal and await a new high-probability setup.

The edge lies in its Positive Net Theta:

consistent time-decay gains protected by Vega

Option Strategy for private portfolios

Apply for Private Desk Access*Membership is strictly limited to ensure quality and direct support.